In the first installment of our series, AI Decisioning’s Triple Advantage for Insurers, we explored how AI decisioning is transforming operational efficiency across the insurance value chain. In this second installment, we dive deeper into a critical operational area where AI decisioning is making a significant impact: insurance fraud detection.

Part 1: How AI Decisioning Fuels Operational Efficiencies in Insurance

Part 3: How AI Decisioning Platforms Enable Insurance Compliance

Or read our ebook Revolutionizing Insurance with an AI Decisioning Platform

The Growing Problem of Insurance Fraud

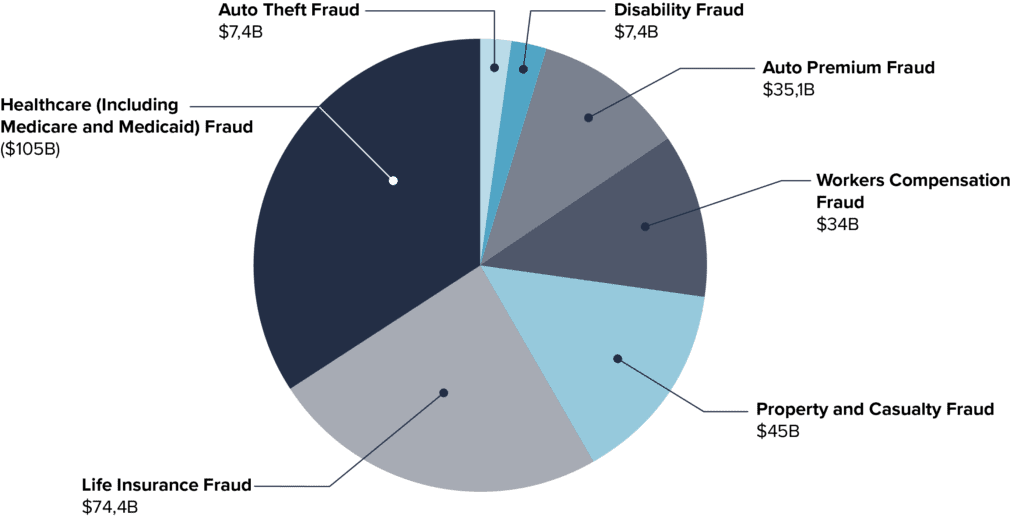

Insurance fraud is a widespread issue, costing U.S. businesses, consumers, and insurers over $300 billion annually in the form of increased premiums and unwarranted payouts. According to the FBI, fraud costs insurers alone $40 billion each year. The growing number and severity of natural disasters, along with fraudsters’ use of technology—especially generative AI (GenAI)—to execute sophisticated schemes, continue to put insurance revenues at risk.

Historically fraud detection has relied on human expertise, manual review and investigation, and inflexible rule-based systems. These methods struggle to keep pace with evolving insurance fraud tactics, resulting in missed or delayed detections. Traditional processes are simply too slow for today’s sophisticated fraud schemes. Insurers need faster and more effective ways to detect when something is amiss.

Enter AI decisioning platforms—tools that leverage machine learning, process automation, and dynamic business rules engines to detect fraud in real time. Insurers that have adopted AI decisioning tools have not only seen a marked improvement in fraud detection rates but also notable gains in operational efficiency and customer satisfaction. This article explains the tangible benefits AI decisioning brings to insurance fraud detection.

Challenges of Traditional Fraud Detection Methods

For decades, insurers have relied on analysts to manually review claims for fraud or have applied preset criteria to flag suspicious activities automatically. This approach presents several challenges:

- Slow processing and inaccuracies: Manually reviewing claims for fraud is time-consuming and prone to human error. Analysts may overlook subtle fraud indicators as they struggle to manually process large volumes of claims. Slow claims processing can also negatively impact customer satisfaction.

- Limited adaptability to new fraud schemes: Many insurers use hard-coded rules such as flagging claims above a certain monetary threshold or those with suspicious characteristics. While these rules can work to some extent, they have limitations. Fraudsters continuously find ways around predefined rules, meaning these inflexible methods often fail to catch new, more sophisticated fraud schemes.

- Higher premiums: Historically, insurers have passed fraud-related losses onto customers in the form of higher premiums. Consumers end up paying an estimated $400-$700 more per year due to fraud-related premium increases. This solution to fraud can drive customers away in this age of transparency and choice.

- Lack of scalability: Traditional fraud detection relies heavily on the experience and intuition of fraud analysts, making it difficult to scale insurance fraud detection whilst ensuring consistent results.

- Insufficient data integration: Human-driven fraud detection methods cannot efficiently handle the vast influx of data from new and varied information sources. This limitation hinders their ability to provide integrated and insightful analyses.

How AI Decisioning Works to Detect Fraud

AI decisioning platforms leverage insurance-related data and predictive analytics to proactively assess fraud risks. Here’s how they work:

- Data integration: AI decisioning platforms ingest and analyze data from numerous sources, such as policyholder information, historical claims data, social media, and external databases (e.g., law enforcement records). This comprehensive data scope allows these platforms to form a clearer picture of claimant and applicant behavior, leading to more accurate insurance fraud detection.

- Machine learning models: These models detect patterns and outliers in large insurance datasets that may indicate fraudulent activity. They can identify subtle trends and correlations that human analysts or hard-coded rules-based systems might miss.

- Continuous learning: Unlike traditional rule-based systems, machine learning models continuously improve over time by learning from new data and adapting to new fraud patterns.

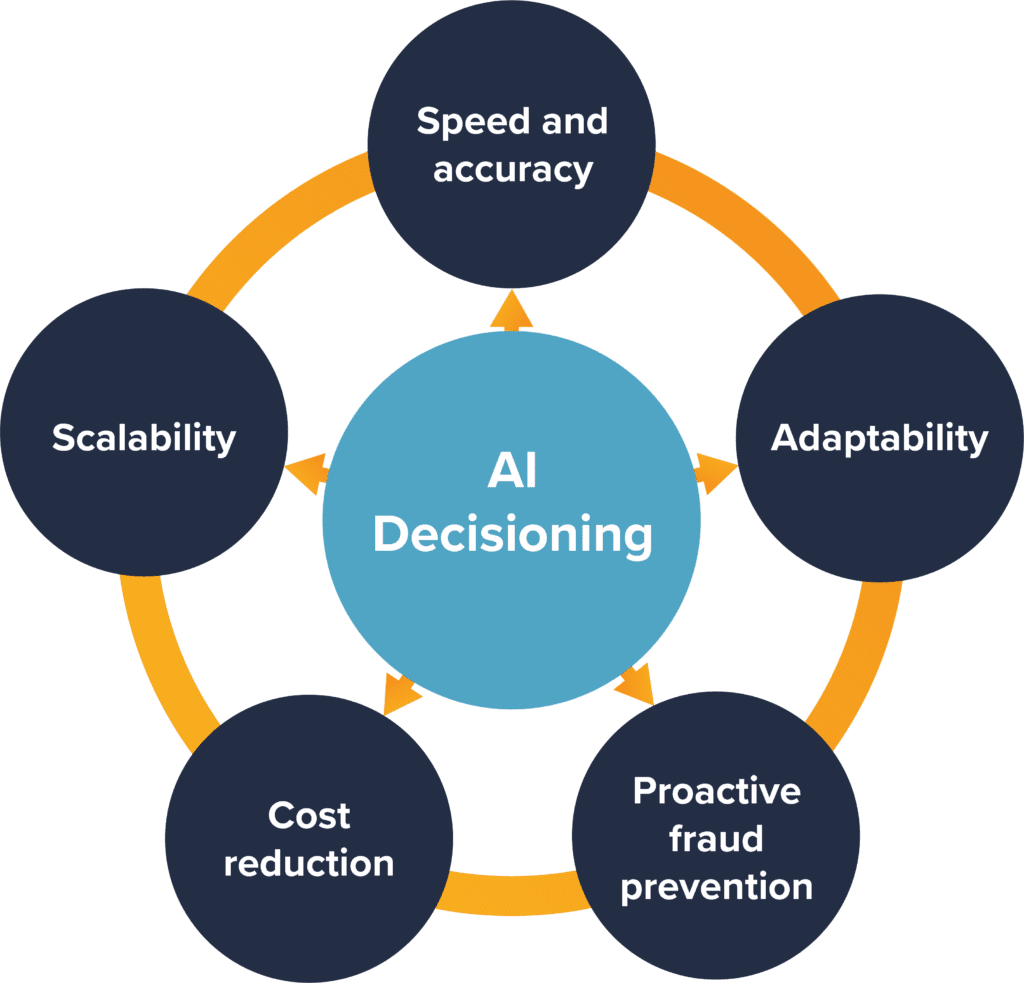

Business Benefits of AI Decisioning for Fraud Detection

From a business perspective, AI decisioning platforms offer significant advantages in fraud detection, including improved speed, accuracy, and operational efficiency.

- Speed and accuracy: Machine learning algorithms detect fraudulent activities with greater precision and speed than human analysts, reducing the time and costs required to process claims. Improved accuracy ensures legitimate claims are processed promptly and fraudulent payouts are minimized.

- Scalability: Automated data analysis and decision-making enable thousands of claims to be processed and analyzed for fraud quickly, consistently, and reliably.

- Adaptability: The low-code nature of AI decisioning tools allows business users to easily create and implement new business rules for claims processing and fraud detection to adapt to emerging threats.

- Cost reduction: By reducing manual work through automation and improving fraud detection, fraudulent payouts are reduced and analyst time is more productive. Additionally, insurers can avoid the cost of customer attrition by keeping premiums attractive.

- Proactive fraud prevention: AI decisioning platforms use predictive analytics and automation to adopt a proactive approach to fraud detection. By analyzing historical data, machine learning models can predict in real-time which policies or claims are more likely to present fraud problems.

AI decisioning platforms are transforming the way insurers detect and prevent fraud and delivering significant business returns in the form of higher detection rates, faster processing, and cost savings. The adaptability of these platforms also ensures that insurers can stay ahead of evolving fraud schemes.

Learn more about how AI decisioning delivers real business benefits to insurers in our ebook “Revolutionizing Insurance with an AI Decisioning Platform.” InRule was recently named a leader in fraud management by CNBC! Read more about it here.